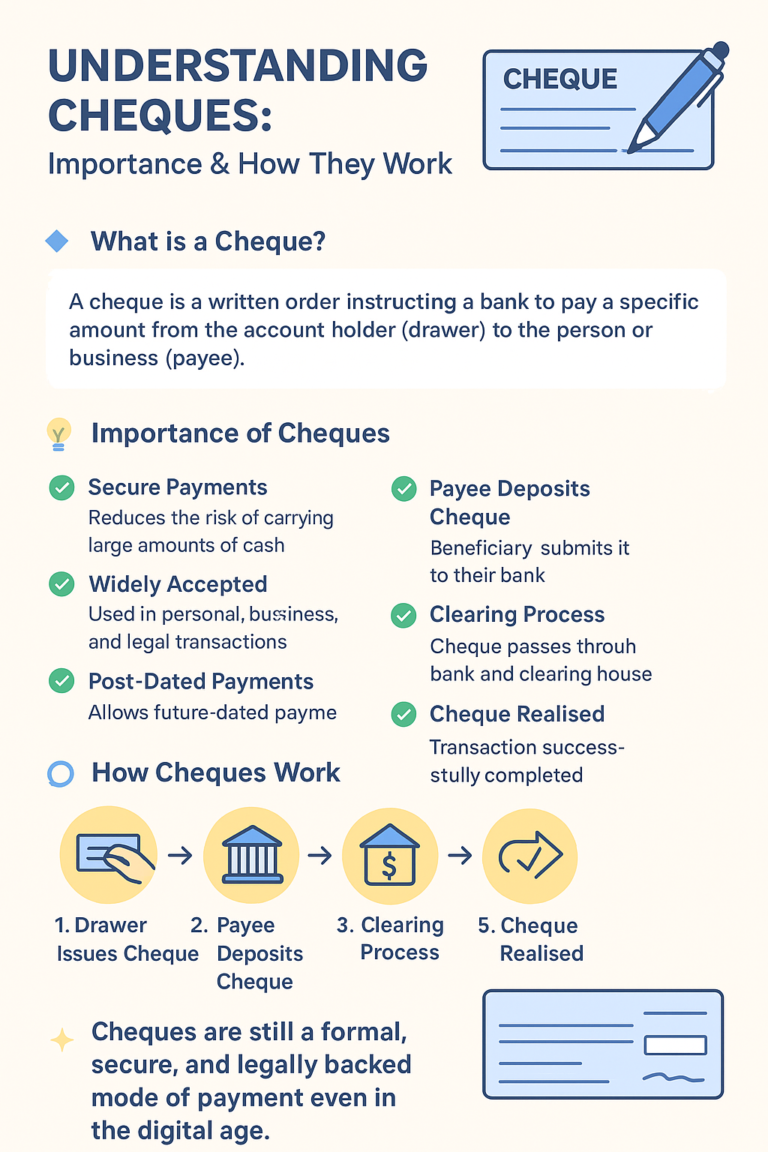

A cheque is a negotiable financial instrument that serves as a written order by an account holder, instructing their bank to pay a specific amount to another person or entity. Unlike cash, which transfers immediately, a cheque functions as a legal promise backed by the banking system. Its power lies in both its practical use in transactions and its legal enforceability under the Negotiable Instruments Act, 1881.

Historical Use of Cheques

The history of cheques dates back centuries. In India, their widespread use emerged during the colonial period, primarily introduced by the British banking system. Over time, cheques became synonymous with trust, security, and professionalism in financial transactions. Until the rise of online banking, they were the backbone of most corporate and personal payments.

Cheques in the Indian Context

Even today, cheques remain crucial in India, especially for:

- Business settlements

- Real estate transactions

- Court-mandated payments

- Salary disbursements in traditional firms

Despite the surge in UPI and digital wallets, the cheque continues to hold ground, primarily because of its legal protection and documentary value.

Understanding Cheques: Importance & How They Work

Role of Cheques in Banking

Cheques are essential to India’s banking system because they offer a structured payment trail. For businesses, they ensure formal record-keeping, and for individuals, they provide a secure non-cash alternative.

Legal Standing of Cheques

Under the Negotiable Instruments Act, a cheque is more than a payment instrument it’s a legally enforceable commitment. If dishonored, the payee can take immediate legal action against the drawer, making cheques a powerful tool for ensuring accountability.

Modern Relevance of Cheques

While digital payments dominate day-to-day expenses, cheques remain indispensable for:

- Court settlements

- Property transactions

- High-value corporate dealings

- Official reimbursements

The key reason? They leave behind undeniable legal proof.

Types of Cheques in India

Cheques are not one-size-fits-all. Depending on their use, Indian law recognizes different types of cheques, each designed for specific circumstances. Let’s break them down:

Bearer Cheques

A bearer cheque is payable to the person who presents it at the bank counter. These cheques don’t require identification the mere possession of the cheque is enough.

- Use Case: Quick withdrawals or informal payments.

- Risk Factor: If lost or stolen, anyone holding it can encash it.

- Example: A business owner issues a bearer cheque to an employee to withdraw petty cash.

Order Cheques

An order cheque is payable only to the person or organization named on it. The bank will cross-check the identity of the payee before releasing funds.

- Use Case: Formal payments requiring proof of delivery.

- Safety Level: More secure than bearer cheques.

- Exampe: A client issues an order cheque in favor of “Intervenor Legal Solutions” for legal services rendered.

Crossed Cheques

These cheques have two parallel lines drawn at the top left corner. They cannot be encashed directly at the counter; instead, the amount must be deposited into a bank account.

- Use Case: Safer business transactions where record-keeping is important.

- Safety Level: High, as money cannot be taken by unauthorized persons.

- Example: A supplier receives a crossed cheque from a corporate client, ensuring direct deposit into their company account.

Account Payee Cheques (A/C Payee Only)

A cheque marked as “Account Payee” restricts payment strictly to the payee’s account. No one else can encash it, even if they have the cheque in hand.

- Use Case: Salary disbursement, vendor payments, or legal settlements.

- Safety Level: Highest among all cheque types.

- Example: An employer issues account payee cheques to employees for monthly salaries.

Post-Dated Cheques

A post-dated cheque is issued with a future date, meaning it cannot be encashed until that date arrives.

- Use Case: EMI payments, rent agreements, or business contracts.

- Risk Factor: If the drawer’s account has insufficient funds on the due date, the cheque may bounce.

- Example: A tenant issues 12 post-dated cheques for monthly rent payments.

Stale Cheques

A cheque is considered stale if it is not presented within 3 months from the date of issue. Beyond this period, banks will not honor it.

- Use Case: Must be avoided by presenting cheques promptly.

- Risk Factor: Delay may render the cheque invalid.

Example: A cheque dated January 1st will become stale if not deposited before April 1st.

Parties Involved in a Cheque

Every cheque transaction involves three primary parties, each with distinct roles and responsibilities:

Drawer

The drawer is the account holder who writes and signs the cheque, directing the bank to pay a specific amount to the payee.

- Responsibility: Ensure sufficient funds in their account.

- Legal Liability: If a cheque bounces, the drawer faces legal consequences under Section 138 of the NI Act.

Drawee

The drawee is the bank that holds the drawer’s account and is responsible for honoring the cheque, provided it meets legal and financial requirements.

- Responsibility: Verify signatures, funds, and cheque validity.

- Limitation: The bank is not liable if the cheque is dishonored due to insufficient funds.

Payee

The payee is the individual or entity to whom the cheque is issued and who ultimately receives the payment.

- Right: To encash the cheque or deposit it into their bank account.

Legal Protection: Can initiate legal proceedings if the cheque is dishonored.

Legal Framework Governing Cheques in India

Negotiable Instruments Act, 1881

This Act is the cornerstone of cheque-related laws, defining obligations, penalties, and protections.

RBI Guidelines on Cheques

The Reserve Bank of India ensures smooth functioning of cheque transactions by issuing standards on clearance, truncation, and fraud prevention.

Supreme Court Interpretations

Over the years, the Supreme Court has strengthened cheque laws, making them more favorable to payees to discourage financial misconduct.

Cheque Bounce: Legal Implications

Reasons for Cheque Bounce

- Insufficient funds

- Signature mismatch

- Post-dated or stale cheque

- Alterations in the cheque

Section 138 NI Act

This section criminalizes cheque dishonor and prescribes punishment of up to 2 years imprisonment or fine up to twice the cheque amount.

Penalties & Punishments

Apart from fines and jail, cheque bounce cases can damage an individual’s or company’s reputation.

Defenses Available

The drawer may argue:

- No legal liability existed

- Cheque was stolen or forged

- Cheque was issued as security, not payment

Cheque Dishonor Procedures

Issuing Legal Notice

The payee must send a written notice within 30 days of cheque dishonor.

Filing a Complaint in Court

If payment isn’t made within 15 days of notice, the payee can approach a Magistrate’s Court.

Time Limits for Action

The complaint must be filed within 30 days of cause of action.

Importance of Cheques in Business Transactions

- Reliability in Deals: Cheques are proof of payment commitments.

- Legal Documentation: Helps in audits and disputes.

- Cash Dependency Reduction: Safer than carrying large sums of money.

Businesses still rely heavily on cheques for bulk transactions.

How Cheques Work in Day-to-Day Transactions

- Issuing a Cheque: Drawer fills out payee details, date, amount, and signature.

- Clearing Process: Cheque moves from payee’s bank to drawee’s bank for verification.

- Settlement: Upon approval, the amount is credited to the payee’s account.

This process is supported by RBI’s Cheque Truncation System (CTS).

Digital Transformation and Cheques

Electronic Cheque Processing

Scanned cheques are processed digitally, ensuring faster clearance.

Cheque Truncation System (CTS)

Eliminates physical movement of cheques, improving speed and reducing fraud.

Digital Alternatives to Cheques

Though UPI, NEFT, and RTGS are growing, they lack the same legal enforceability as cheques.

Comparing Cheques with Other Payment Methods

- Cheques vs. Cash: Cheques offer safety and traceability.

- Cheques vs. Online Banking: Online is faster but less reliable in legal disputes.

- Cheques vs. UPI Payments: UPI is instant, but cheques are enforceable in courts.

Preventing Cheque Fraud

- Common Scams: Forged signatures, altered cheques, fake banking instruments.

- Preventive Measures: Always cross cheques, use “A/C Payee,” and keep records.

- Legal Remedies: Victims can file FIRs and pursue civil as well as criminal remedies.

Role of Lawyers in Cheque-Related Disputes

- Legal Consultation: Lawyers guide clients on NI Act compliance.

- Litigation for Cheque Bounce: Filing cases under Section 138.

- Advisory for Businesses: Drafting corporate cheque policies to avoid disputes.

Intervenor Legal Solutions specializes in swift resolution of cheque disputes.

Understanding Cheques for Individuals

- Personal Finance Management: Cheques help keep track of spending.

- Safe Practices: Use account-payee cheques for security.

- Avoiding Legal Hassles: Maintain sufficient balance and avoid post-dated misuse.

Understanding Cheques for Businesses

- SMEs: Use cheques for vendor payments and salaries.

- Large Companies: Manage bulk transactions.

- Record-Keeping: Cheques serve as legal financial documents.

Case Studies of Cheque Disputes in India

- Court Judgments: Landmark cases emphasize strict action against defaulters.

- Lessons Learned: Courts lean in favor of honest payees.

- Future Precedents: Uphold trust in financial instruments.

Why Cheques Are Still Relevant Today

- Trust Factor: Seen as more reliable than digital wallets.

- Legal Safeguards: Stronger than online transfers.

- Acceptance: Widely recognized in formal transactions.

The Future of Cheques in India

- RBI Policies: Push for digital systems.

- Decline in Usage: Urban consumers shifting to UPI.

- Possible Replacements: E-cheques and blockchain systems may emerge.

Common Myths About Cheques

- Cheques Are Outdated: Still used in businesses.

- Cheques Are Unsafe: Crossed cheques are among the safest instruments.

- Cheques Have No Legal Value: Legally binding under NI Act.

Tips for Writing a Valid Cheque

- Avoid alterations or overwriting.

- Always sign consistently with bank records.

- Ensure sufficient funds before issuing.

Intervenor Legal Solutions: Expertise in Cheque Matters

Why Choose Intervenor Legal Solutions

Delhi’s best law firm with a strong reputation in cheque-related litigation.

Successful Case History

Handled numerous high-value cheque bounce cases with favorable outcomes.

Client-Centric Legal Advice

Personalized guidance for individuals, SMEs, and corporates.

Conclusion

Cheques are more than financial tools they are legal instruments that guarantee accountability in transactions. While digital payments dominate, cheques continue to play a crucial role in India’s business and legal framework. For expert handling of cheque disputes, Intervenor Legal Solutions stands as Delhi’s most reliable law firm, trusted by individuals and businesses alike.

FAQ

Frequently Asked Questions

Three months from the date of issue.

Yes, within the cheque’s validity period.

Yes, under Section 138 NI Act.

Yes, by issuing a stop-payment request to your bank, but it may attract legal liability.

Immediately inform your bank and file a complaint.

Yes, under RBI’s Cheque Truncation System.